How to select a commercial property for investment

Tom Dean • January 26, 2021

Choosing wisely

There are many considerations to take into account when deciding what commercial property to invest in.

Deciding on what your priorities are and what the right strategy is for you, is key to long term success. Commercial real estate investing is not "get rich quick," but it is "get rich for sure" if done correctly.

With that said, here are some of the main considerations that you need to think about.

Management intensiveness

Commercial real estate is not always a passive investment, and most of the time it will require significant time and effort to make it work. One of the key things when considering the property is how much time you want to commit to the property and how it will fit with other areas of your life.

For instance, self-managing a single tenant industrial building on a long term triple net lease will require very little time compared to a 20 unit multifamily building. Multifamily, in general, will be more hands-on than just about any other class. This can be mitigated by using a property manager to take care of the "tenants, toilets and termites" associated with multifamily, but this usually requires many units to make sound financial sense.

Office has historically been a low maintenance asset class. However, with the changes in recent years towards more co-work, and short term leases, these assets require more care than ever before. Similarly, retail requires little time to manage, but if a plaza has some vacancy or occasionally takes on pop-ups, this will need more management to run successfully.

Industrial assets and land leases are generally the most hands-off when it comes to management. Most industrial leases will place much of the responsibility for the maintenance squarely on the tenant, often using "net and care free" leases to put the entire burden of property management back onto the tenant.

Again, management intensiveness goes down dramatically with a property manager. This will make the most sense to established investors and those with large portfolios, as time will become their number one consideration and priority with their buildings.

Single-tenant vs. multi-tenant

Single versus multi-tenant buildings will also form a significant consideration for most investors. A single tenant operation often requires less time to manage than a building with multiple tenants, but there are serious tradeoffs in this equation.

Most notably, the single-tenant scenario creates a lot of vacancy risk for the owner, and in a commercial context, a single vacancy can a long time to fill once the tenant has vacated. If you own a 12,000 sqft retail plaza, and you lose a tenant, chances are you still have a majority of tenants paying you rent while you fill the space, and you'll continue to service the debt without an issue. If you have a 12,000 sqft industrial building with a single tenant - and you lose that tenant - you have 100% vacancy and no income to service debt.

The same goes for residential investors. The single-family home is great when it's leased, but when you lose that tenant, you must scramble to get someone in quickly or risk losing all of the gains you've built up since purchasing the property. If you're a multifamily owner and have even just a fourplex, your prognosis is much better if you lose a tenant, and the others will be able to carry much of the property's cost while you fill the vacancy.

Financial Covenant

The financial covenant (the strength of the tenant) is both a positive and a negative feature. Every sensible landlord will want a tenant who can pay rent and has a history of successful operation behind them. A long and proven track record and solid references from past landlords can serve to give the new landlord a comfort level with existing tenants – this is a good thing.

Historically, the strongest covenant has been the "national" brand, a company with multiple locations and a national or international presence. Where you can run into issues with these tenants is when they decide not to pay. The landlord will still have recourse in the event of non-payment, but if this is a major tenant (a single-tenant scenario or an anchor tenant such as a grocery store for a retail plaza), they may have the ability to outlast the landlord in a legal battle. If a billion-dollar company decides not to pay you, you may be hard-pressed to collect compared to smaller operators.

As the saying goes, fools rush in where angels dare to tread.

Risk and return

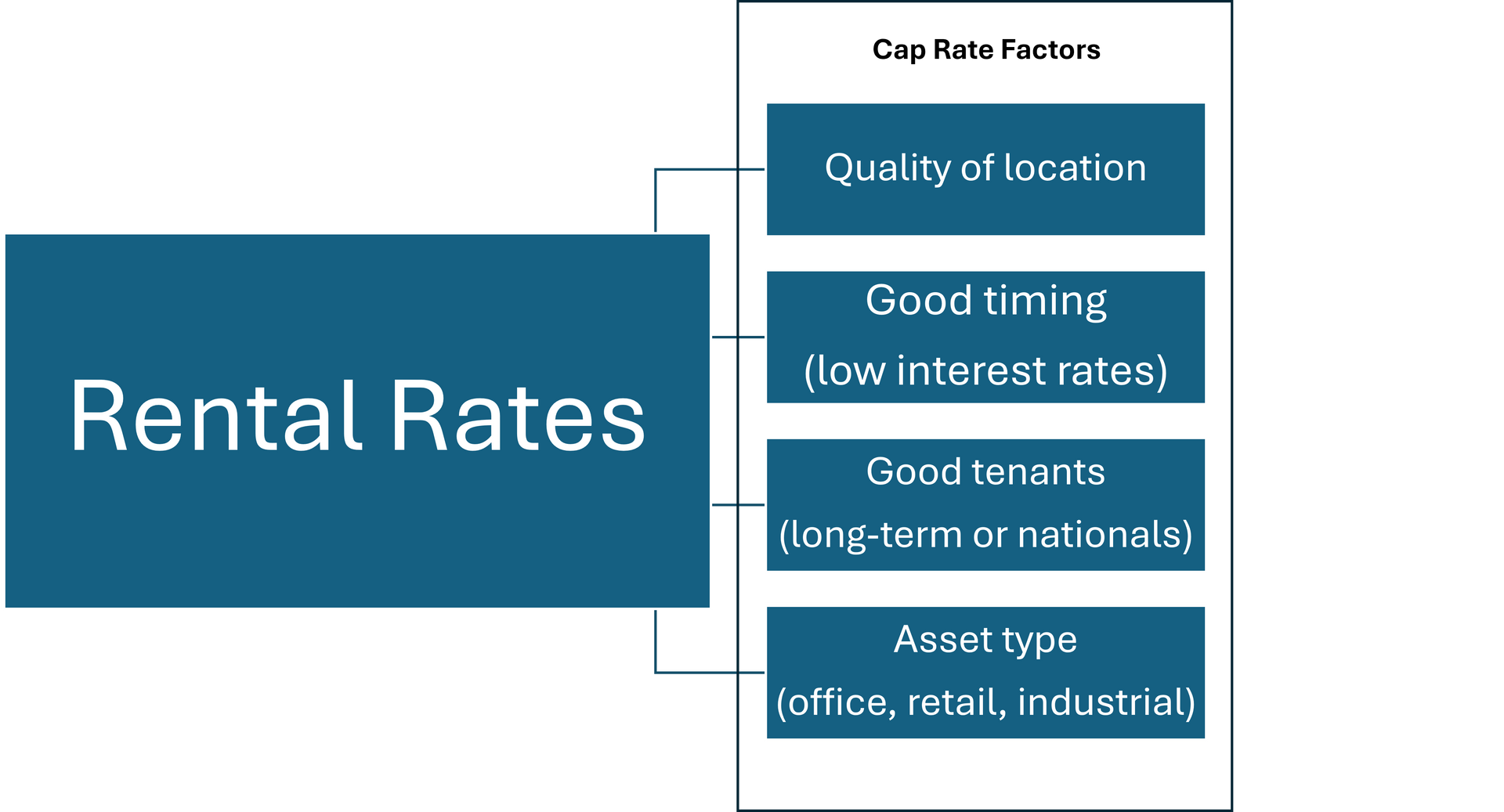

A very successful real estate investor once told me that, if he had to do it over again, he would have purchased more properties with a lower cap rate.

To new investors, this will seem counterintuitive because the cap rate indicates the rate of return on the property, but the reality is that it also suggests the risk. For example, many small-town investment properties will trade at a high cap rate, often in the mid-teens. This is a high rate of return. Bit, it assumes that everyone pays their rent, that tenants continue to rent, that things go well for the town (many small towns are dependent on a single sector or industry such as oil, forestry, pulp, mining, etc. so if the town loses its primary industry, it may take decades to recover). So, assuming everything goes perfectly, this is an excellent investment. But, the moment things go sideways, not only does the asset lose value, its liquidity goes out the window as well.

A lower cap rate indicates a smaller return, but if it's a realistic price, then typically, these are well managed, highly desirable locations with strong fundamentals and lower risk. It also means that there will be greater liquidity for the product when the time comes to sell. It's also likely that the property will have a higher average lease term and will be less management intensive due to crime or vacancy issues.

If you've ever seen the start of Schitt's Creek, the reason that the government seized all the family's assets but not the 4,500-acre town they owned is because of the hilarious illiquidity of the asset, and the governments inability to sell the property either! It was a boat anchor, and had no value without substantial work.

Cap rate matters, but what matters more is the owner's ability to service the debt and come out ahead on the investment. Overall, the investment has to "make sense."

Appreciation or cash flow

Another consideration with the investment is whether appreciation or cash flow is the strategy. There are ways to do both, but when investors talk about appreciation vs cap rate, they're talking about something more specific. If you make a great play, the asset will appreciate and cash flow.

However, this strategy refers explicitly to how the property will be run, on what time horizon, and the projected exit (disposition or an eventual sale of the property).

For example, let's suppose a cash flow investor buys a retail plaza that's had decent management over the years and still have some useful life. They may decide that the best strategy is to do only maintenance which is absolutely necessary, and pull out their money over time. The goal may be to depreciate the property to virtually zero, and sell as a redevelopment to someone who will then turn around the property. When this investor goes to sell, the property will almost certainly be worse off than when they bought it.

This is where the appreciation investor comes in. This is someone who perceives an "upside" or "value add" in a particular asset and buys it with the expectation of realizing value on a pre-determined time frame. This investor may purchase the same retail asset, now distressed, with deferred maintenance issues and vacancy, expecting to fix the problems and add value. They may improve the façade of the building, improve common areas, and fix long-standing issues. The goal may be to sell the property (flip) quickly or it may be to add value, increase rents, and hold long term, or refinance the property once the value is realized.

There's no right or wrong method, but each of these will have its own particular challenges and long-term implications to an investor. Chances are an appreciation type investor will receive more community support than a cash flow investor, who may come to be seen as a slum landlord.

In conclusion

The right asset to invest in is dependent on the buyer. Each buyer must take specific considerations into account that will be completely different than every other investor. Factors such as lifestyle, personal expertise/past employment, business history, willingness to commit time to the investment.

If you'd like to have a conversation with one of our team, about what can work for you, please reach out to me at tom@lizotterealestate.com

New to the game? Check out:

https://grantcardonetv.com/channel/realestateinvestingmadesimple/

https://www.biggerpockets.com/podcast

http://commercialrealestatepodcast.com/adam-paul-first-capital/

Edmonton physicians: how to buy your clinic building with no down payment using physician-specific financing from RBC, TD, and Scotiabank.

How can you maximize the value in your commercial property? This article lists three main ways to improve your value.

This article talks about healthcare specific real estate considerations, and how to build a team, and occupy the best possible space for your practice.

What are cap rates and how do they affect real estate values? Read this article to find out.

This is an article about how best to position, and make decisions on disposing of commercial real estate assets.

A description of how leaseback transactions work in commercial real estate.